GS III: Challenges to Internal Security through communication networks; Basics of Cyber Security; Awareness in the fields of IT, Computers.

Reason Why It Was In News

Importance from UPSC Exam Perspective

Featured due to the alarming rise in cybercrimes (900% jump) and scams (APK, Digital Arrest) targeting Indians, particularly those originating from Southeast Asia, necessitating a strong government response.

Critical for understanding contemporary threats to national security and the digital economy, and evaluating government countermeasures and technological solutions.

Definitions/Introduction

What is Cybercrime?: Cybercrime encompasses activities where a computer or network is the target, the means, or the victim used to commit or facilitate a crime.

Core Concept

Definition/Context provided in Sources

Digital Fraud/Scam

Crimes that exploit human psychology—fear, greed, urgency—through social engineering tactics like phishing, vishing, smishing, and fake government impersonation to steal financial or personal data.

APK Scam

Financial fraud driven by malicious Android Package Kit (APK) files, often disguised as official portals, which install malware to steal data, banking credentials, and OTPs, bypassing official app stores.

Digital Arrest

A cyber scam where fraudsters impersonate law enforcement via video calls, threatening fake arrests to coerce victims into paying large sums of money.

Operational Technology (OT) Security

Hardware and software systems controlling physical processes, such as electric grids and pipelines, which form the backbone of critical infrastructure. Digital integration of OT and IT systems has created a major vulnerability or “dangerous blind spot” in security.

Mule Accounts

Accounts, enabled by weak Know Your Customer (KYC) procedures, used for layering and dispersal of funds, making fund recovery extremely difficult.

Historical Evolution / Background / Timeline

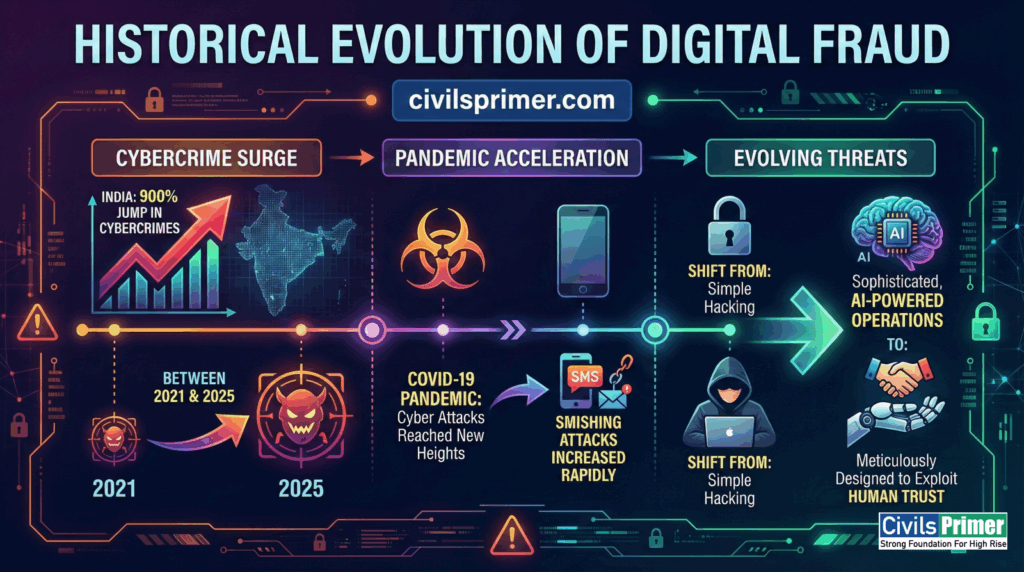

Cybercrime Surge: India has witnessed an alarming 900% jump in cybercrimes between 2021 and 2025.

Pandemic Acceleration: During the COVID-19 pandemic, cyber attacks reached new heights, with smishing attacks increasing rapidly.

Evolving Threats: The sources highlight a shift from simple hacking to sophisticated, AI-powered operations meticulously designed to exploit human trust.

Historical Evolution of Digital Fraud – for UPSC Notes

Constitutional / Legal / Institutional Framework

Framework Element

Provision / Nodal Agency

UPSC Prelims Tip

Legal Backbone

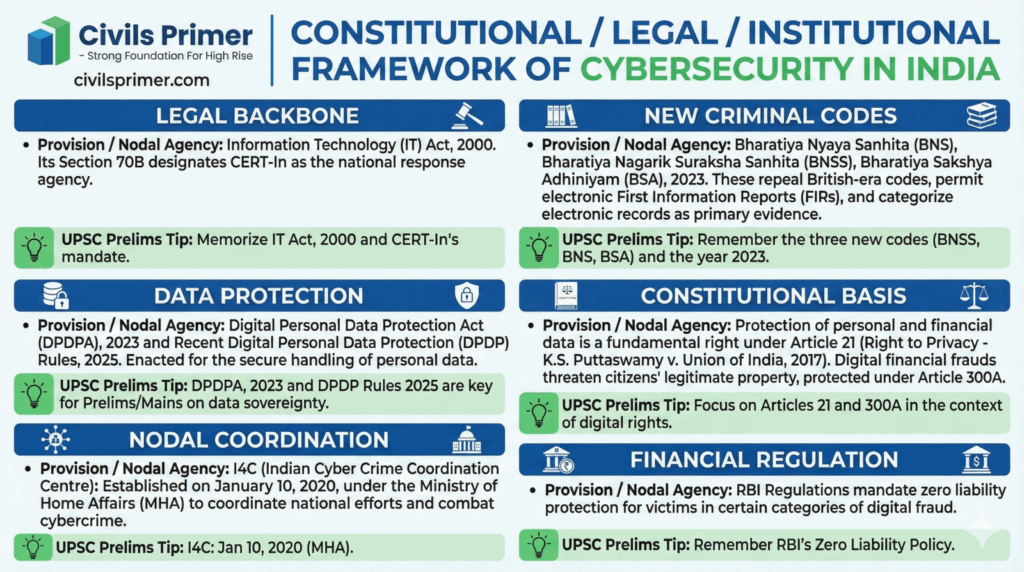

Information Technology (IT) Act, 2000. Its Section 70B designates CERT-In as the national response agency.

Memorize IT Act, 2000 and CERT-In’s mandate.

New Criminal Codes

Bharatiya Nyaya Sanhita (BNS), Bharatiya Nagarik Suraksha Sanhita (BNSS), Bharatiya Sakshya Adhiniyam (BSA), 2023. These repeal British-era codes, permit electronic First Information Reports (FIRs), and categorize electronic records as primary evidence.

Remember the three new codes (BNSS, BNS, BSA) and the year 2023.

DPDPA, 2023 and DPDP Rules 2025 are key for Prelims/Mains on data sovereignty.

Constitutional Basis

Protection of personal and financial data is a fundamental right under Article 21 (Right to Privacy – K.S. Puttaswamy v. Union of India, 2017). Digital financial frauds threaten citizens’ legitimate property, protected under Article 300A.

Focus on Articles 21 and 300A in the context of digital rights.

Nodal Coordination

I4C (Indian Cyber Crime Coordination Centre): Established on January 10, 2020, under the Ministry of Home Affairs (MHA) to coordinate national efforts and combat cybercrime.

I4C: Jan 10, 2020 (MHA).

Financial Regulation

RBI Regulations mandate zero liability protection for victims in certain categories of digital fraud.

Remember RBI’s Zero Liability Policy.

Legal Framework of Cybersecurity in India

Government Initiatives & Policies (Domestic)

The government has undertaken several institutional, legal, and technological measures to address cybercrime:

Indian Cyber Crime Coordination Centre (I4C) Network: Launched the Suspect Registry (a centralized database of cybercrime suspects) and the Cyber Commandos programme.

Citizen Financial Cyber Fraud Reporting and Management System (CFCFRMS): This centralized system, accessible via the 1930 helpline and the National Cybercrime Reporting Portal (NCRP), facilitates coordination between law enforcement agencies, major banks, and telecom companies for immediate action to prevent the loss of money in real-time. The system has successfully saved over ₹3431 Crore across 9.94 lakh complaints.

Technological Tools for Fraud Prevention:

The RBI Innovation Hub developed MuleHunter.AI, an AI-powered model designed to reduce digital fraud by identifying and dealing with “mule” bank accounts.

Sanchar Saathi is a portal that allows citizens to check their mobile connections, verify the genuineness of handsets, and report suspicious calls or fraudulent connections.

Infrastructure & Awareness:

The exclusive ‘bank.in’ domain for domestic banks minimizes cybersecurity threats and strengthens trust in digital banking.

The government implements awareness campaigns through SMS, social media, Cyber Dost, and digital displays.

CyTrain is an online platform that trains over 98,000 police and judicial officers on investigating and prosecuting cybercrime.

Evaluation (Mains Perspective):

Global Legal Frameworks

UN Convention Against Cybercrime (2024): Adopted by the UN General Assembly and signed by 72 nations, this convention establishes the first universal framework for prosecuting online offenses, including ransomware and financial fraud.

India’s Position: India has not yet signed the UN Convention Against Cybercrime. This stance is consistent with its past refusal to sign the Europe-led Budapest Convention on Cybercrime. India’s reservation stems from concerns over data sovereignty, privacy, and a preference for a framework that aligns better with its national legal standards, particularly the Puttaswamy ruling on data protection.

International Cooperation: India participates in global operations like Interpol’s Operation HAECHI-VI, which focuses on disrupting cyber-enabled financial crime and money laundering. This specific operation led to the blocking of over 68,000 bank accounts. India has also invoked the Mutual Legal Assistance Treaty (MLAT) with countries to facilitate investigations and the exchange of evidence for crimes like cyber fraud.

Issues, Challenges & Gaps

Explosive Growth and AI Sophistication: The 900% surge in cybercrimes is exacerbated by AI, which enables personalized phishing, deepfake voice/video scams, and polymorphic malware that constantly changes its code to evade traditional antivirus programs.

Cross-Border Jurisdictional Challenge: The majority of large-scale financial fraud networks operate internationally, often from Southeast Asia, exploiting jurisdictional gaps and making tracing and recovery difficult.

Vulnerability of Critical Infrastructure (OT): Critical infrastructure relies on Operational Technology (OT) systems which lack adequate cybersecurity investment. Firms spend 10 times more on IT security than OT security, creating a “dangerous blind spot” in industrial control systems.

Mule Accounts and Money Laundering: Weak KYC compliance allows mule accounts to be created and used for rapidly layering and dispersing fraudulent funds, undermining the recovery process.

Digital Divide and Victim Profile: Cybercriminals often target vulnerable populations, particularly the elderly and rural citizens, who are financially susceptible but lack the necessary digital literacy to recognize sophisticated social engineering attacks.

Under-equipped Law Enforcement: Cyber police often lack the necessary manpower, specialized training, and AI-driven tools required to effectively investigate complex digital crimes.

Institutional Negligence in Finance: Banks frequently fail to detect and flag abnormal, high-value transactions, which allows scams to progress.

Evolving Regulatory Landscape: India’s cautious stance on international treaties like the UN Convention Against Cybercrime and the Budapest Convention risks limiting its access to global cooperation channels and real-time intelligence sharing.

Concise Case Studies

Case Study

What Happened, Why It Matters, & Lesson

Digital Arrest Scam (2025)

A 78-year-old retired banker lost ₹23 crore in 2025 after being subjected to a “digital arrest” scam where fraudsters impersonated law enforcement via video calls. Lesson: This illustrates the high financial impact and the effective use of social engineering combined with official impersonation to exploit the fear factor, particularly targeting high-net-worth or elderly individuals.

APK Scam (FatBoyPanel)

Fraudsters circulate malicious APK files designed to mimic official government portals (e.g., subsidy schemes) through social media. When installed, these apps steal critical banking credentials, OTPs, and personal data in real-time. Lesson: This shows how criminals leverage the Android ecosystem to spread malware outside regulated app stores and target citizens by exploiting trust in government initiatives.

Ransomware Spike

India recorded a sharp 55% hike in ransomware incidents, with 98 attacks recorded in 2024. Lesson: This indicates the increasing focus of cybercriminals on disrupting systems to extort money. The risk extends to critical infrastructure, where downtime can cost millions.

Key Reports to Cite

Report Title

Year

Main Finding Cited in Sources

NCRB Crime in India Report

2023

Cybercrimes rose sharply by 31.2% to 86,420 cases, with nearly 69% involving online fraud.

Digital Threat Report

2024

Deepfakes and AI-generated content are noted as potent tools for intrusion, particularly in social engineering attacks.

Cybercrime Report

2024

Global cyberattacks on infrastructure cost an estimated $10.5 trillion annually.

World Economic Forum (WEF) Report

2024

Only 15% of cybersecurity professionals specialize in OT systems, highlighting a severe skill gap in critical infrastructure protection.

Stakeholders & Their Roles

Stakeholder

Role in Cybersecurity & Fraud Management

Government (MHA, MeitY, DoT)

Coordinates national response (I4C), manages incidence response (CERT-In), defines legal/regulatory framework (IT Act, DPDPA), and secures communication networks (Sanchar Saathi).

RBI & Banks

Implements zero liability policies, enforces KYC norms, deploys technological defenses like MuleHunter.AI to detect mule accounts, and is mandated to monitor abnormal transactions.

Private Sector/Platforms

Includes tech platforms and payment apps (TIUEs) now subject to the Telecommunications (Telecom Cyber Security) Amendment Rules, 2025, requiring compliance with verification and suspension orders.

Citizens

Must enhance digital literacy, exercise caution against social engineering, and utilize official portals (NCRP, 1930) for timely complaint registration.

International Partners (Interpol, UN)

Provide platforms for global cooperation, intelligence sharing (like Operation HAECHI-VI), and the development of universal legal standards.

Best Practices & Models

Technological Proactivity: Employing AI/ML for real-time anomaly detection and personalized transaction profiling is crucial for early fraud prevention, as demonstrated by the RBI’s MuleHunter.AI model.

Critical Infrastructure Defense: The World Economic Forum recommends adopting Internal Network Security Monitoring (INSM) models to mandate real-time OT traffic surveillance, recognizing that OT systems require governance separate from traditional IT.

Institutional Coordination: The CFCFRMS (1930 helpline) model, which links banks, telecoms, and law enforcement on a single platform for immediate fund freezing, is a proven best practice for minimizing financial loss.

Targeted Awareness: Launching targeted digital literacy campaigns specifically for senior citizens and rural communities helps counter the vulnerability exploited by social engineering scams.

Way Forward / Reforms / Recommendations

Priority Reform

Action / Rationale

Institutional & Capacity Building

Establish 24/7 cyber rapid response units and expand forensic labs. This strengthens the capacity of law enforcement (LE) to meet the scale of rising crimes, moving from passive reporting to active pursuit.

Financial Accountability

Strictly enforce KYC compliance and penalize banks for failing to monitor abnormal transactions or freeze mule accounts quickly. This shifts the burden of security from citizens to financial institutions.

Cross-Institutional Data Fusion

Build a National Fraud Intelligence Grid linking banks, telecoms (using Sanchar Saathi data), and LE agencies to enable rapid attribution and track international fraud networks.

OT Security Mandate

Mandate minimum security standards (like WEF’s INSM model) for critical infrastructure/OT systems, closing the current dangerous blind spot and protecting physical processes.

Global Engagement

Enhance Interpol cooperation and sign bilateral cyber treaties (MLATs) to improve tracking of cross-border criminal enterprises originating from regions like Southeast Asia.

Introduction: Define cybercrime (where computer is means/target) and state the urgency (e.g., 900% jump 2021-2025).

Challenge Paragraph 1 (Socio-Technological): Focus on AI-enabled threats (deepfakes, polymorphic malware) and social engineering targeting digitally illiterate citizens.

Challenge Paragraph 2 (Institutional & Governance): Discuss the cross-border origin of scams (Southeast Asia focus), prevalence of mule accounts, and the critical OT security blind spot.

Policy Response (Legal/Institutional): Cite the new criminal laws (BNS, BNSS, BSA, 2023), the role of I4C/CERT-In, and real-time intervention through the CFCFRMS (1930).

Recommendations/Way Forward: Prioritize mandatory bank accountability, AI/ML deployment (MuleHunter.AI), and strengthening international MLAT cooperation.

Conclusion: Emphasize the shift from reactive redressal to proactive, AI-driven prevention and the necessity of digitally literate citizens for a resilient digital economy.

Prelims Revision Pack (Crisp Facts)

Institution/Act

Facts

I4C

Indian Cyber Crime Coordination Centre; established January 10, 2020.